Your home loan EMI could drop further if RBI keeps cutting rates

RBI August Pause: Will Your EMI Fall Further?

🤯 A 0.25% rate cut on a ₹40L home loan saves you ~₹650/month — that's 130 cups of chai...

▼▲Read Full StoryCollapse

The RBI's rate-setting committee meets August 3-5 and economists expect it to hold rates steady after cutting earlier in 2025. If rates stay put, your EMIs won't change this month — but the bigger question is what happens to your loan costs for the rest of the year.

The RBI Monetary Policy Committee is scheduled to meet August 3-5, 2025 to review the benchmark repo rate and overall policy stance.

Most economists expect the MPC to hold rates steady at this meeting while maintaining a cautious tone on inflation going forward.

The RBI has already delivered three rate cuts in 2025, giving floating-rate borrowers meaningful EMI relief over the past few months.

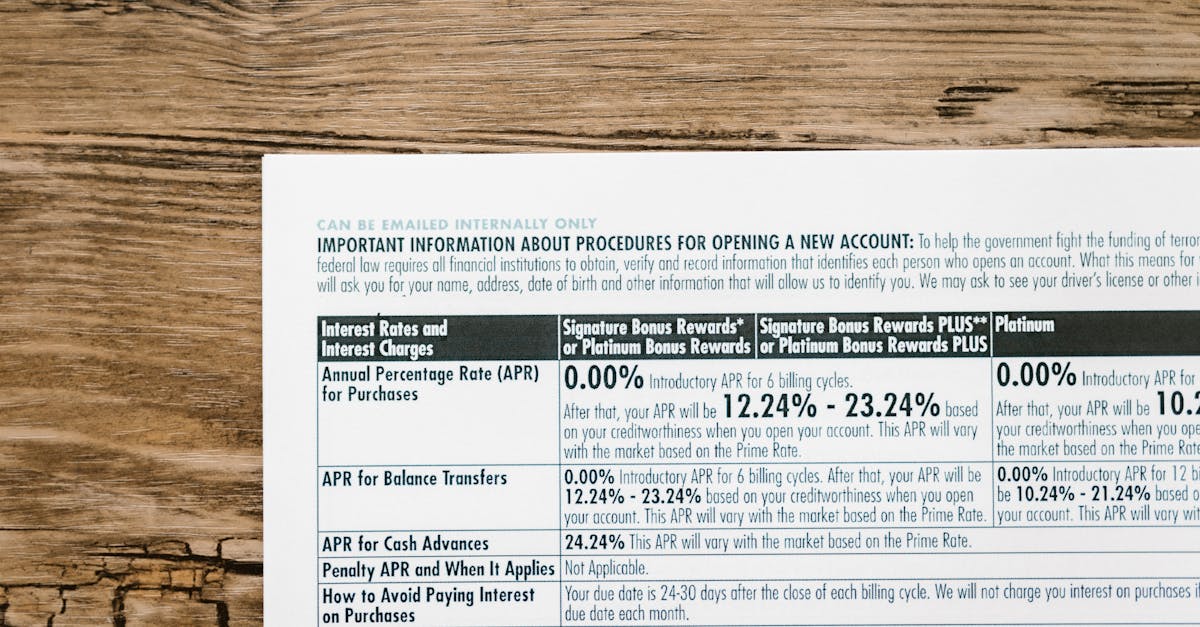

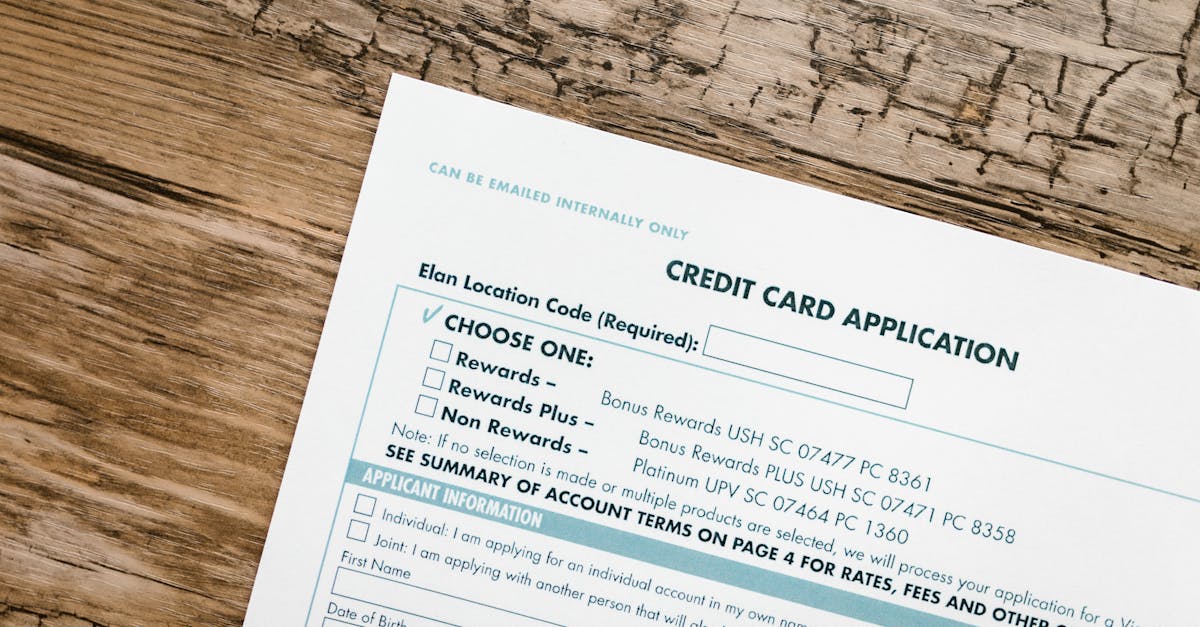

Check whether your home or personal loan is linked to the repo rate — if it is, confirm your bank has already passed on the previous 0.75% cuts to your EMI or outstanding principal.

Compare your current loan interest rate against new offers in the market — a rate hold period is the best time to refinance or negotiate a reset with your lender without missing further cuts.

Review your FD and debt mutual fund strategy: a prolonged rate pause means existing long-term FD rates are still attractive, so lock in now before any future cuts reduce deposit yields.

Pro tip: Banks are not required to automatically reduce your EMI after a repo cut — call your lender and explicitly request a rate reset or principal adjustment, especially if your loan was taken before 2019.

RBI rules change your EMI — check your current rate

Compare Rates →